Is The Bond Bull Over? Not Quite!

The bull market in bonds is over… or is it? There has been much ballyhoo the past couple of weeks about the bull market in bonds being over if rates get to a certain level. Just a quick refresher, bonds act like a teeter-totter with bond values on one side and bond rates on the other side. The fear for bond investors is that if the rate side rises, the value side goes down. So in one’s effort to make money, price going down makes it really hard! Two very successful bond managers have recently traded barbs about knowing the 30 year bull market in bonds will be over if rates get to X or if rates get to Y. One manager suggests the bull market in bonds would be over if rates got to 2.6%, while our second bond manager suggests the bull market would be over if the interest rate got to 3%. Oh, those whacky finance guys!

I don’t like using terms like bull and bear, but I’m sticky with it for this week. Most associate bull markets has an upward trajectory in price and a bear market is the opposite. I’m just assuming when our two large, egomaniacal bond managers start talking about a bear, a movement down in price is what I think they are saying. It is true that interest rates have fallen about 90% since the early 1980’s. And since my base case scenario is that we don’t go to negative interest rates here in the U.S., 90% is pretty close to 100%, so it makes sense to wage such a bet that the bull market is over. However, they are not thinking about a third option (hint: this has been my base case scenario for some years now). So prices, or in this case yields, can only do three things. That’s it! I’m not sure why humans try to make this stuff harder then it is. Things can go up, go down or go sideways. My base case scenario is that the bond market goes sideways for a long time – like 15 or 20 years.

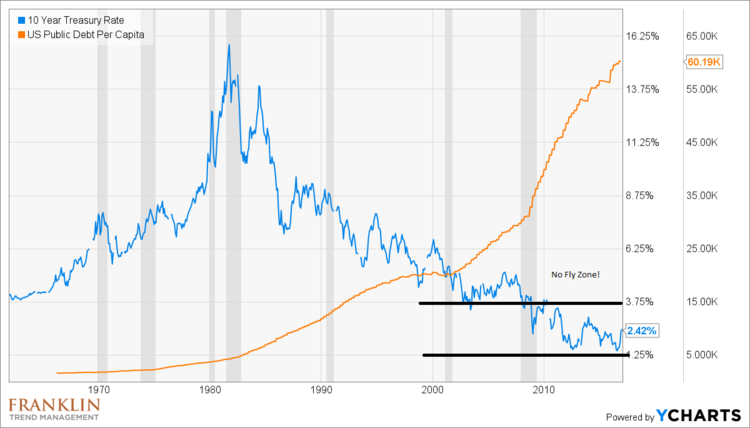

If we now draw our attention to the graphic above, I’ve presented a long-term view of ten-year treasury yields – about 60 years worth of data. The problem with a real bear case for bonds is the orange line. The orange line is roughly each person’s responsibility for our current level of debt (this is just on the books US Government debts – not including off-balance sheet obligations or personal consumer debt). If I included everything, our $60k number probably goes up 3 to 5 times. I like the per capita figures because the debt levels become understandable. No one really comprehends what trillions looks like. The problem with rates getting too high is that the economy goes negative – really negative. The interest on our debt obligations gets really out of whack with potentially declining tax revenues.

As you can see, our current debt level, while certainly ramped higher over the past 8 years, has been increasing at a fast pace for a long time. In the 60’s and 70’s, debt per capita was around $2k. High rates on our current debt levels is just not going to happen. So what about growth? Can’t we just grow our way out of our obligations? Yes we can, but the economy has this funny way of going down sometimes. As long as the government let’s the economy do its thing, we can eventually grow our way out of the level of debt. If the government massively cuts back on a lot of discretionary programs, we can grow our way out of our debt. If the government makes some significant changes to health care and social security spending, we can grow our way out our debt. Here is a crazy idea! How about not expanding the current debt level by 7% YoY (which is over twice the rate at which our economy grows, btw)?

The answer to growth is getting our economy back into its height-weight-proportional (HWP) area. To do this will take some time – like a decade or two. Expect rates to stay in a wide trading range up to 3.75%(ish) down to 1.25%(ish) for many, many years. Bonds will have to be traded in the future if you expect to make any money in this segment of the capital markets. Most individual investors are just not thinking this way.

Humbly,

P. Franklin, Jr.

January 22nd, 2017

All opinions and estimates included in this communication constitute the author’s judgment as of the date of this report and are subject to change without notice. This communication is for informational purposes only. It is not intended as an offer or solicitation with respect to the purchase or sale of any security. This information is subject to change at any time, based on market and other conditions. Any forward looking statements are just opinions – not a statement of fact.

Investing may involve risk including loss of principal. Investment returns, particularly over shorter time periods are highly dependent on trends in the various investment markets. Past performance does not guarantee future results.