Capital Markets WIR - Are Stocks In A Bubble?

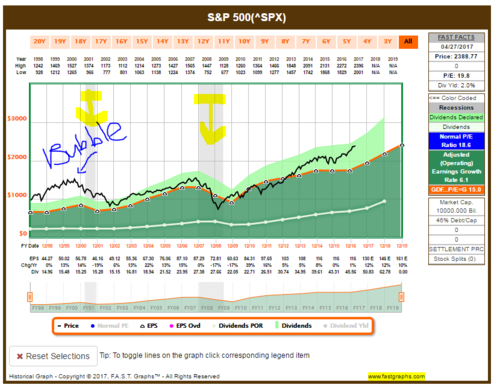

Pictured above is a price graph of the S&P 500. I'm not a fan of indexes, especially this one, but it is what everyone looks at so I'm going with it. Like people, all assets have a certain mass that they can reasonably carry around with them. For people you sometimes see a height-weight chart (HWP) and in stocks, one measure (not the only one!) of this height-weight analysis is the price to earnings ratio (P/E). Now, I'm not going to make any kind of argument that you must buy at a low P/E to make money in stocks. It is really the future P/E that you should be focused on anyhow! So, what are a few take-aways from this chart?

First, stocks follow earnings. More importantly, stock prices are a refection in confidence about future earnings. If the orange line in the graph above is a fixed 15 times earnings, you can see that the black line (price) will fall ahead or rise above in anticipation of changes in the orange line (fair value line). The long-term, fair value line will act similar to a magnet pulling in price. Again, it may take years for this relationship to play out, so using this analysis as a basis for buying and selling in the market is not wise.

Second, valuations don't matter until they do matter. The fact that stocks are priced at 20 times earnings or 10 times earnings is not predicative. The P/E is probably best used like a wind sock on an airstrip. The current multiple of earnings is simply saying we are in a zone that is above a long-term fair value multiple. That's it. Do not get into labels of expensive or cheap. It will affect your thinking and lead you down a wrong path. Don't be an Alan Greenspan calling an audible in December of 1996 about the silliness of irrational exuberance only to watch stocks double in price over then next three years. Have rules about how to successfully operate in the market. Think of the P/E multiple like a thermometer. It simply reads back to you the temperature. It is NOT a thermostat! You cannot use P/E multiples to control or predict future prices.

Third, is that recessions are bad for stock prices. Duh! I've highlighted a couple of the last recessions on this chart. You can see again, stocks anticipated the recession by declining ahead of time. Now, for the perma-bull, indexers out there, a recession is coming. There will be a sharp contraction in the business cycle and equities will not be spared. Given the excessive liquidity created by the Fed, I would not be surprised if the decline in stocks was more severe than normal. So if the run of the mill bear market declines by 40%, I wouldn't be surprised by a decline of more than 50% from the ultimate high. I recently had a conversation with a client, who I consider to be, a very well-read and experienced investor. I honestly just mentioned this relationship in passing and he was in disbelief that I would be modeling a 50% or greater decline in stock prices. While the probabilities are currently low, they will increase over time. It is just what happens and there is not much anyone can do about it. I cannot stress enough the importance of having a crisis plan BEFORE the crisis not during the crisis.

Last, we are no where near bubble valuations. As you can see on the chart, stock prices were stratospheric in 1999. All stock prices pull value forward. Stock prices are the, "I'll gladly pay you Tuesday for a hamburger today," of assets. So in 1999, stocks pulled forward about 13 years of earnings. Again, stocks are elevated in price, but after considering dividends, they currently don't seem that expensive to me.

Best returns!

P. Franklin, Jr.

April 28th, 2017

All opinions and estimates included in this communication constitute the author’s judgment as of the date of this report and are subject to change without notice. This communication is for informational purposes only. It is not intended as an offer or solicitation with respect to the purchase or sale of any security. This information is subject to change at any time, based on market and other conditions. Any forward looking statements are just opinions – not a statement of fact.

Investing may involve risk including loss of principal. Investment returns, particularly over shorter time periods are highly dependent on trends in the various investment markets. Past performance does not guarantee future results.