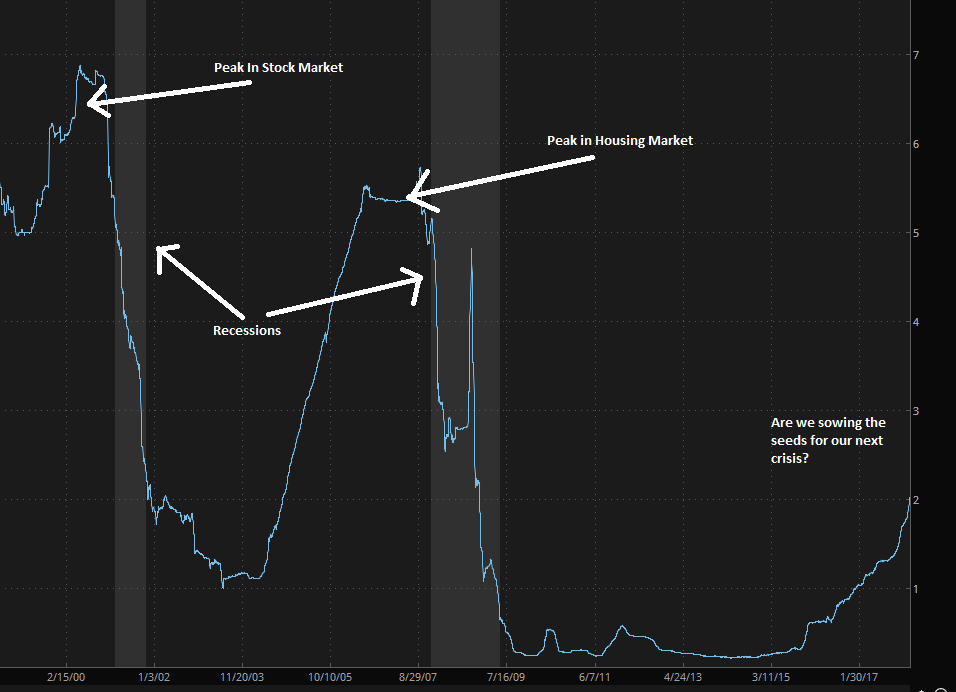

The graph above is an image of the 3-Month LIBOR, based in U.S. Dollar. This is a key benchmark for short term interest rates. This is the interest rate that large financial institutions pay to borrow funds. Customers (you and me) will pay a mark-up from this rate when they borrow.

So interest rates have been kept artificially low for far too long based on the totally baked idea (and widely accepted by most economists) that by moving around key interest rates that some how these "levers and knobs" will create changes in individual's appetite for risk taking. The foolish notion that by dropping rates will create demand is really, well...dumb.

But, here we are! Almost 6 years of low to zero to negative back to low interest rate environment only sows the seeds for the next crisis. Isn't it ironic that the government's solutions to past problems only seem to create the next crisis? We should all take a moment to ponder that one!

Anyway, it would not surprise me if 2018 was termed "LIBOR's Revenge!" This spells all sort of issues for of assets that are based on credit. The top of this list is residential real estate. Next on the list would be US pension funds, and then I suppose I'd throw in Life & Annuity Insurance Companies just for good measure.

Cheers,

P. Franklin, Jr.

March 15th, 2018

All opinions and estimates included in this communication constitute the author’s judgment as of the date of this report and are subject to change without notice. This communication is for informational purposes only. It is not intended as an offer or solicitation with respect to the purchase or sale of any security. This information is subject to change at any time, based on market and other conditions. Any forward looking statements are just opinions – not a statement of fact.

Investing may involve risk including loss of principal. Investment returns, particularly over shorter time periods are highly dependent on trends in the various investment markets. Past performance does not guarantee future results.